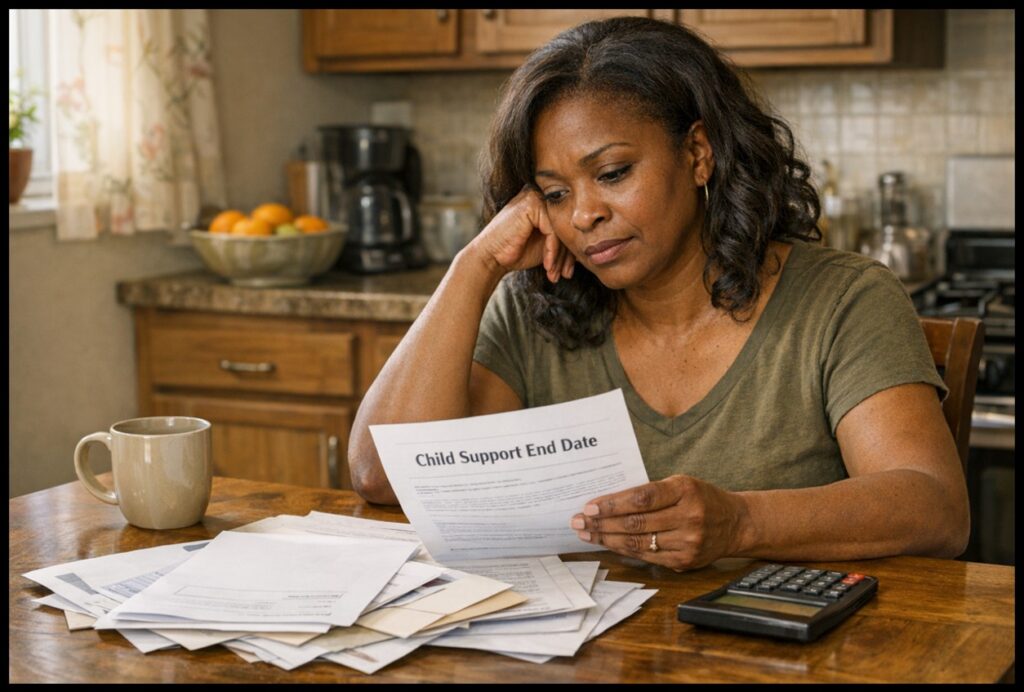

When the clock hits midnight on your child’s eighteenth birthday, it’s amazing how fast your bank account feels the shift. For almost two decades, that monthly or bi-weekly child support deposit was part of your household rhythm, right up there with rent, lights, and groceries. Then suddenly…it’s gone. Meanwhile, your child is still eating like there’s a team to feed, the bills have not shrunk, rent is still due on the first, and now college letters may be piling up on the counter. But that financial help you counted on through the court system? Gone.

This moment is what many people call the “child support cliff”, that sudden financial drop that can turn a proud milestone into a stressful scramble. It’s a lot, and if you’re feeling overwhelmed, that makes sense. But with a little planning and a steady approach, you can get through this transition. Let’s talk about how to handle it with confidence.

Understanding the Legal Blueprint

To move through this shift with a little less stress, it helps to understand the system behind it. Child support laws exist for a pretty straightforward reason, children have a legal right to financial support from both parents, no matter what the relationship between the parents looks like. The goal is to make sure the cost of raising a child; food, shelter, healthcare, and education, is shared as fairly as possible.

In most cases, the system is built around the idea that once a child turns 18, they are legally old enough to work and begin stepping into adulthood. That is why child support often ends at that point, although the exact rule depends on your state and your court order.

Navigating the Extension Maze

Now, here’s the part a lot of people do not realize: the cutoff is not always set in stone. In some situations, support can continue longer, but you usually have to ask for that extension before the current order ends.

Extensions are usually granted when:

- Your child is still in high school or enrolled full‑time in college (support may continue until age 19–23).

- Your child has a severe physical or mental disability that prevents financial independence, in these cases, support can sometimes continue indefinitely.

If you think your situation may qualify, do not wait until the last minute. File early so you are not scrambling later.

What to Do When Collection is a Battle

If collecting support has always felt like a full-time job, the end date can make everything feel even heavier. But here is the good news: unpaid back child support does not disappear just because your child turns 18.

Your state’s Child Support Enforcement agency can still help collect what is owed. Depending on the situation, they may be able to:

- Garnish wages

- Intercept tax refunds

- Seize lottery winnings

- Place liens on property

- Suspend driver’s licenses

- Even pursue jail time

If the agency is moving slowly, a private family law attorney may be able to help you push things forward by filing a contempt motion or taking other legal steps to collect what you are owed.

The Proactive Countdown: When to Prepare

Waiting until the last check arrives to adjust your budget can leave you in a real bind. A better move is to start preparing about twelve to eighteen months before support is scheduled to end. That gives you time to do a little financial practice run while you still have a cushion. Take a look at how much of your monthly income child support covers, then start making small changes now. Maybe that means trimming a few fixed expenses, building your emergency fund, or testing what life looks like without relying on that money as heavily. The more you prepare ahead of time, the less overwhelming the transition will feel later. Let’s walk through a few ways to get ready.

- Assess Your Financial Situation

The first thing to do is take an honest look at your finances. That means looking at your income, monthly bills, debts, and savings without judgment, just clarity. Put together a detailed budget that shows where your money is coming from and where it is going. Once you see everything in one place, it gets a whole lot easier to spot what needs attention and where you may be able to cut back.

- Adjust Your Budget

Once child support ends, your budget has to reflect your new reality. Start with the basics, housing, utilities, groceries, transportation, and anything else that absolutely has to be paid. Then take a close look at the extras. Dining out, entertainment, subscriptions, and impulse spending may need to be trimmed for a while. Budget apps and spending trackers can help, but even a simple notebook works if that is what you will actually use.

- Increase Your Income

If you can, look for ways to bring in a little more income to help cover the gap. That might mean a part-time job, freelance work, selling a skill you already have, or starting a small side hustle. You can also think about asking for a raise or applying for a better-paying role if that makes sense for you. A little extra income can make a big difference when you are trying to stabilize your household.

- Build an Emergency Fund

An emergency fund matters even more during a transition like this. Try to build up at least three to six months of living expenses in a separate savings account if you can. That money becomes your cushion for the stuff life throws at you, car repairs, medical bills, reduced work hours, all of it. Start small if you need to. Even a little bit set aside consistently adds up overtime.

- Pay Down Debt

If you are carrying debt, now is a good time to make a plan for it. Credit cards, personal loans, and medical bills can eat up money you are going to need elsewhere. Focus on paying down the balances with the highest interest first if possible. You can also look into consolidation or payment arrangements if that would give you more breathing room.

- Plan for the Future

Even while you are handling today’s bills, do not lose sight of your long-term goals. Retirement, education costs, and big future expenses still matter. If you are able, keep contributing to retirement savings like a 401(k) or IRA, and look into options for college savings if that is part of your plan. You do not have to do everything at once, but keeping the future on your radar helps you stay grounded.

- Seek Professional Advice

If all of this feels overwhelming, getting professional advice can really help. A financial advisor can help you create a plan that fits your real life, not just some generic checklist. They may also help you think through savings, debt, investments, and the bigger picture so you can make decisions with more confidence.

- Stay Positive and Focused

This transition can be stressful, no question. But try not to let fear make every decision for you. Stay focused, set realistic goals, and give yourself credit for the progress you make along the way. Financial stability is not built overnight, but with planning and consistency, you can absolutely create it.

Ways to supplement lost income after child support has ended

When that money does stop coming in, replacing it usually takes a mix of flexibility, creativity, and strategy. Here are some realistic ways to help fill the gap without losing your mind in the process:

- Monetize Existing Assets: If you have a spare bedroom or a vehicle you do not use all the time, renting it out could bring in extra income with relatively little effort.

- The Sublimation and Customization Market: If you are crafty and creative, a small customization business could be a solid side hustle. Personalized shirts, mugs, tumblers, and home décor can be made from home and on your own schedule once you have the right equipment and supplies.

- Healthcare Support Roles: Training for a role like a home health aide can open the door to flexible work that is often in demand. It can be a practical option if you need shifts that fit around another job or family responsibilities.

- Independent Travel Consulting: If you are great at planning and organizing, helping people book travel can become a low-overhead online business and a nice source of commission-based income.

- Freelance Remote Services: Writing, bookkeeping, virtual assistance, customer support, and other remote skills can all turn into freelance income. If you enjoy creating content, blogging or affiliate marketing may also be worth exploring over time.

- Drive for a Rideshare Service: If you have a reliable car and some free time, driving on your days off can be a flexible way to bring in extra money. Most services require an application and background check.

- Become a Medical Courier Driver: Medical couriers deliver prescriptions, lab materials, and secure documents for healthcare providers. It can be another solid option if you want flexible driving work and do not mind a background check.

- Have Your Adult Children Contribute if They Still Live at Home: If your child is now an adult and still living at home, it may be time for a conversation about contributing to the household. That could mean helping with one bill, groceries, or another regular expense as they learn financial responsibility.

Conclusion

If your chest feels heavy right now, take a breath. Look at the amazing human you raised. You made it through sleepless nights, school plays, scraped knees, and all the pressure that comes with holding a household together. The end of child support is a financial shift, yes, but it is also a milestone. You helped guide your child into adulthood, and now it is your time to regroup, rebuild, and steady your finances for what comes next.

This next chapter is not about lack; it is about adjustment. With some planning, a realistic budget, and a proactive mindset, you can move through this transition with confidence and create a secure future on your own terms. You have carried so much already, and you are more capable than you think. Do not give up, you’ve got this.